Compute inventory by tracking units, valuing costs, and applying FIFO, LIFO, or average.

If you want to master how to compute inventory, you’re in the right place. I work with operators, founders, and accountants who need clear steps that hold up in audits. In this guide, I explain how to compute inventory from the ground up, with simple formulas, real examples, and tips I use in month-end closes.

What counts as inventory (and what does not)

Inventory includes items you plan to sell or use to make goods. That means raw materials, work in process, and finished goods. It can also include packing supplies that ship with the product. It does not include office supplies, tools, or assets used to run the business.

Set clear rules for what you track as a SKU. Use consistent units and names. When you learn how to compute inventory, this setup is your base. Clean masters make every later step faster and more accurate.

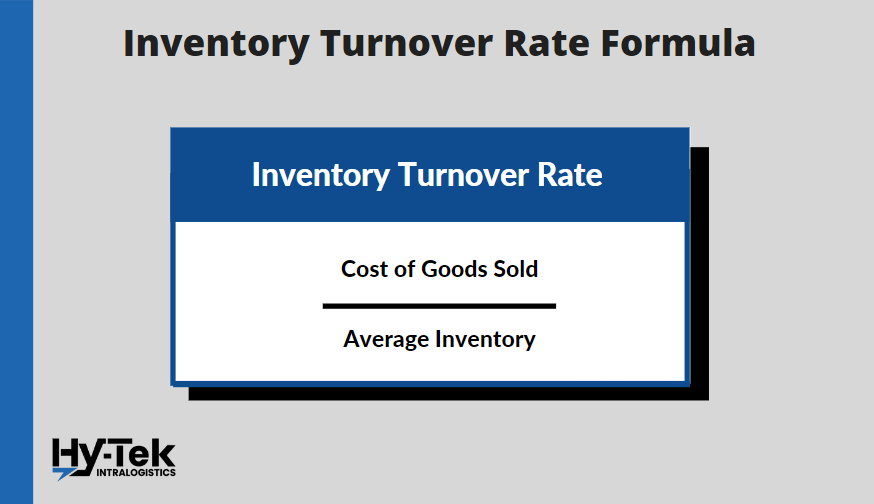

Core formulas you will use

Here are the staple formulas I use in every close. Learn these, and how to compute inventory becomes much easier. Keep them in your close checklist and template.

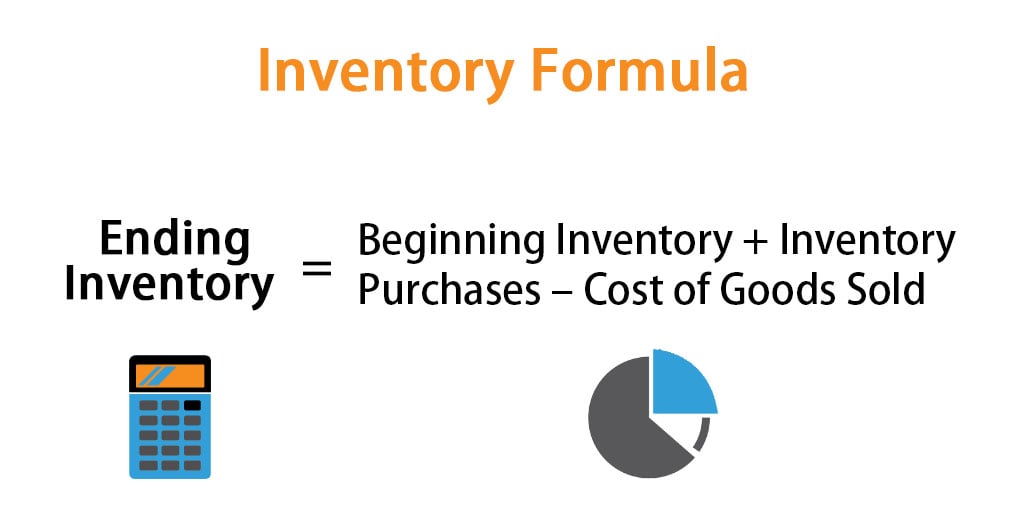

- Cost of goods sold (COGS): Beginning inventory + Purchases + Freight-in − Purchase returns/discounts − Ending inventory.

- Ending inventory (periodic): Count units on hand × unit cost under your chosen method.

- Cost of goods available for sale: Beginning inventory + Net purchases.

- Average cost per unit (weighted average): Cost of goods available for sale ÷ Units available for sale.

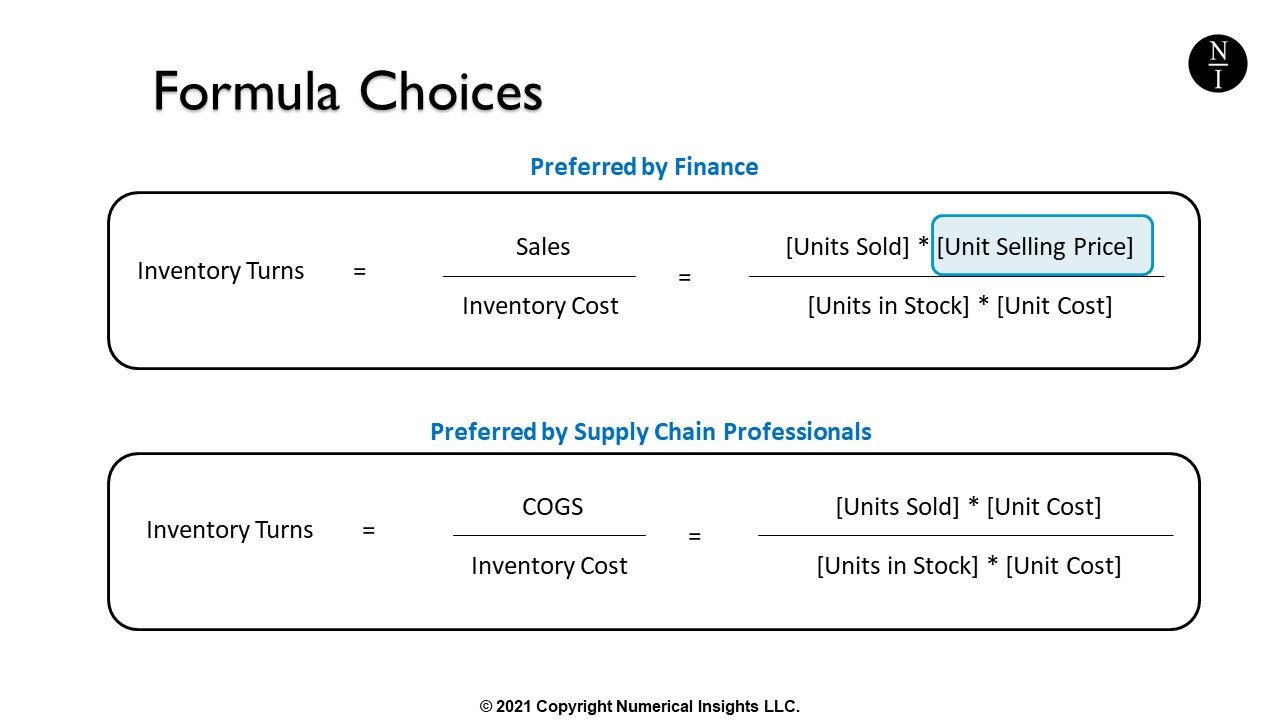

- Inventory turnover: COGS ÷ Average inventory. Days on hand: 365 ÷ Turnover.

Let’s try a quick example. You start with $10,000, buy $25,000, and end with $8,000. COGS is $27,000. If average inventory is $9,000, turnover is 3.0, and days on hand is about 122.

Inventory valuation methods: FIFO, LIFO, weighted average, specific ID

Choosing a method is a core part of how to compute inventory. It changes COGS and tax timing. It also shapes margins and the story your numbers tell.

- FIFO (First-In, First-Out): Oldest costs go to COGS first. Ending inventory uses newer costs. In rising prices, FIFO gives higher ending inventory and lower COGS.

- LIFO (Last-In, First-Out): Newest costs go to COGS first. Ending inventory uses older costs. In rising prices, LIFO gives lower ending inventory and higher COGS. Note: Allowed under US GAAP but not under IFRS.

- Weighted average: Smooths price swings. Compute one average cost per unit for the period or after each receipt (perpetual average).

- Specific identification: Track exact costs for unique items (cars, art, custom jobs). Best when units have clear, separate costs.

Mini example for FIFO: Suppose you bought 100 units at $10 and then 100 units at $12. You sold 150 units. Under FIFO, COGS = 100×$10 + 50×$12 = $1,600. Ending inventory = 50×$12 = $600.

Periodic vs perpetual: two ways to keep the books

This is a key choice in how to compute inventory day to day. A periodic system updates COGS at the end of the period. A perpetual system updates COGS with each sale.

In a periodic system, you count units at month-end. Then you apply your cost method to the count. You compute COGS with the core formula. This works well for small teams, but it needs a good physical count.

In a perpetual system, software posts inventory and COGS as you buy and sell. You still do cycle counts to adjust for shrinkage. This gives real-time data for decisions and cash planning.

Step-by-step: how to compute inventory for month-end close

Follow these steps. I use this flow with clients to speed up close and reduce errors.

- Lock the cut-off. Stop shipping and receiving at a set time. Make sure all orders are posted.

- Count or cycle count. Scan or count units on hand by SKU and location. Investigate big gaps right away.

- Clean purchases. Post freight-in, duty, and vendor credits. Flag consigned or customer-owned stock.

- Choose the method. Apply FIFO, LIFO, weighted average, or specific ID. Use your policy and stay consistent.

- Price the count. Multiply counted units by the right cost per unit. Sum to get ending inventory.

- Compute COGS. Use the core formula. Reconcile to your sales and margins.

- Book adjustments. Record shrinkage, write-downs, or reclass. Add notes that explain the why.

- Review KPIs. Check turnover, days on hand, and gross margin for sanity.

If you want to learn how to compute inventory without stress, build a repeatable checklist. Keep a versioned workbook and tie every number back to a source. That habit speeds audits and new team onboarding.

Practical tips and mistakes I see

From my own closes, here are items that often save the day. They look small, but they add up to a clean result.

- Do a soft freeze. Pause changes during counts. Moving stock mid-count causes messy gaps.

- Track landed cost. Add freight, duty, and handling to item cost. Missed landed costs can gut margins.

- Check cut-offs. Match receipts and shipments to the right period. Bad cut-offs skew COGS.

- Watch slow movers. Mark down items that will not sell at cost. Use lower of cost or net realizable value.

- Compare to last month. Large swings in units or prices need a story. Write two lines to explain.

I once found a 3% shrinkage at a 3PL because the team used mixed units. The fix was simple. We added unit-of-measure checks to the receiving sheet. If you ask how to compute inventory that passes audit, start with clean units.

Advanced: manufacturing and overhead

If you make goods, how to compute inventory includes more steps. You must capture materials, labor, and overhead into work in process and finished goods.

Use a bill of materials and a routing. Post materials at standard or actual cost. Apply labor and overhead with a clear rate. At month-end, true up standards to actuals, and book variances.

Overhead rates should reflect real drivers. Use machine hours, labor hours, or cost drivers that make sense. Document your basis and update it when the shop changes mix or volume.

Inventory analysis and KPIs that matter

How to compute inventory does not end at the balance. It continues with fast checks on health. These metrics help you tune cash and service.

- Inventory turnover and days on hand: Show speed of sell-through.

- Service level and fill rate: Show if stock levels meet demand.

- GMROII (gross margin return on inventory investment): Gross margin dollars ÷ average inventory dollars.

- Aging by SKU: Spot dead stock early.

- Forecast error: Ties planning to real results.

Set targets by category. High-velocity items need tight control and frequent counts. Slow movers may need price action or bundles.

Tools and templates to speed the work

Even simple tools help a lot when you learn how to compute inventory. Start with a clean spreadsheet and clear tabs.

- Data tabs: Beginning inventory, purchases, receipts, sales, and counts.

- Keys: SKU, lot, location, unit of measure, and dates.

- Cost tab: Cost layers for FIFO/LIFO, or rolling average calc.

- Output: Ending inventory, COGS, KPIs, and a sign-off page.

If you use software, set rules for landed cost, units, and approvals. Test your reports against a hand-built month. This helps catch setup issues before they hurt your numbers.

Frequently Asked Questions of how to compute inventory

How do I choose between FIFO, LIFO, and weighted average?

Pick based on your goals, price trends, and rules you must follow. FIFO is common and simple, LIFO may lower taxes in rising prices under US GAAP, and average smooths swings.

How often should I count inventory?

Do cycle counts weekly and a full count each quarter or year. Short, regular checks reduce year-end pain and improve accuracy.

What if my physical count does not match the system?

Investigate big gaps, then book a shrinkage adjustment. Next, fix root causes like units, receiving errors, or cut-off issues.

Can I use LIFO outside the United States?

Most countries using IFRS do not allow LIFO. If you operate across borders, align with local rules and your tax team.

How do I handle returns in inventory?

Inspect and grade returns fast. If sellable, return to stock at cost; if not, write down or scrap.

How to compute inventory for e-commerce with 3PLs?

Sync receipts and shipments daily and do joint cycle counts. Reconcile 3PL reports to your ledger and book variances each month.

When should I write down inventory?

When net realizable value is below cost due to damage, obsolescence, or price drops. Document the reason and method to support the entry.

Conclusion

You now know how to compute inventory with clear steps, clean formulas, and smart checks. Set strong masters, pick a method, price your count, and test KPIs. Keep a simple, repeatable process, and your numbers will earn trust.

Start this month with a checklist and a small cycle count. Then build from there. If this helped, subscribe for more guides, or leave a question and I’ll share a template you can use.