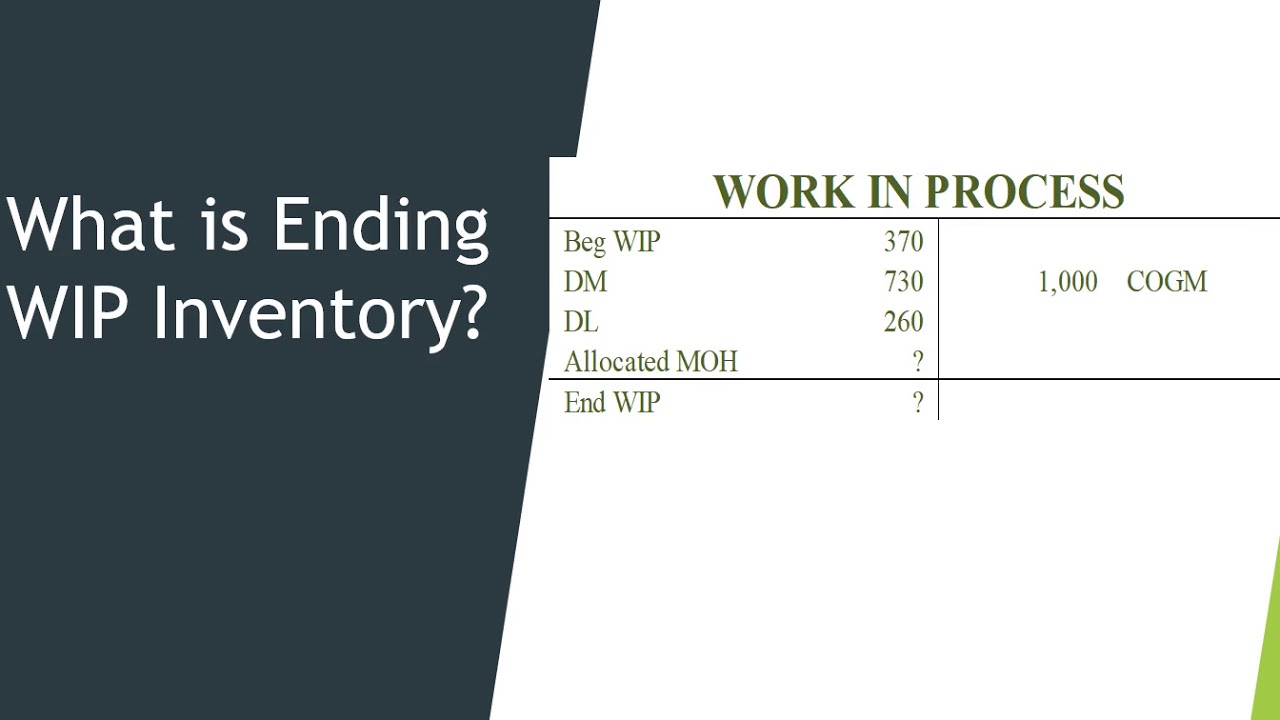

Ending WIP = Beginning WIP + Costs Added − Cost of Goods Manufactured.

If you want clean financials and smarter production decisions, you need to master how to calculate work in process ending inventory. I’ve helped factories, food processors, and custom shops fix month-end chaos with a simple, proven approach. In this guide, I’ll walk you through how to calculate work in process ending inventory step by step, with clear examples, common pitfalls, and tips from real closes.

What Is Work in Process and Why It Matters

Work in process (WIP) is the cost of units that are not yet finished at period end. It sits between raw materials and finished goods. It includes direct materials, direct labor, and manufacturing overhead for partially made items.

WIP affects your margins, your balance sheet, and your shop floor focus. When you know how to calculate work in process ending inventory, you can spot delays, avoid overproduction, and trust your numbers.

The Core Formula for WIP Ending Inventory

Here is the basic formula many teams use to calculate WIP:

Ending WIP = Beginning WIP + Total Manufacturing Costs − Cost of Goods Manufactured

What each term means:

- Beginning WIP: The value of unfinished work at the start of the period.

- Total Manufacturing Costs: Direct materials used + Direct labor + Applied manufacturing overhead for the period.

- Cost of Goods Manufactured (COGM): The cost of units finished and moved to finished goods this period.

This formula works best when you track what got completed. If you make continuous goods, add one more layer: percent of completion. That is where equivalent units come in. You still follow how to calculate work in process ending inventory, but you adjust for stage of completion.

Step-by-Step: how to calculate work in process ending inventory

Follow these steps at month end. Keep the steps simple, and your numbers tight.

- Gather inputs

- Beginning WIP balance.

- Materials issued to production.

- Direct labor booked to jobs or departments.

- Overhead applied this period.

- Units completed and transferred out.

- Units still in process and their percent complete for materials and conversion.

- Compute total manufacturing costs

- Add direct materials used + direct labor + applied overhead.

- Find cost of goods manufactured

- Use production reports for units completed.

- If you use equivalent units, compute cost per equivalent unit, then multiply by units completed.

- Plug the formula

- Ending WIP = Beginning WIP + Total Manufacturing Costs − COGM.

Simple numeric example:

- Beginning WIP: 10,000

- Direct materials: 50,000

- Direct labor: 30,000

- Overhead applied: 20,000

- Total manufacturing costs: 100,000

- COGM: 90,000

- Ending WIP = 10,000 + 100,000 − 90,000 = 20,000

Many readers ask how to calculate work in process ending inventory when units are only part done. Use equivalent units and the same formula. The idea is the same, but COGM and ending WIP are split by degree of completion.

Job Order vs Process Costing: Pick the Right Approach

Your path depends on how you make products.

Job order costing

- Used for custom work or batches.

- Track costs by job: materials, labor, overhead.

- Ending WIP is the sum of open job balances at period end.

Process costing

- Used for continuous or high-volume lines.

- Use equivalent units to handle partial completion.

- Two common methods: Weighted-average and FIFO.

Weighted-average equivalent units:

- Equivalent units for materials = Units completed + Ending WIP units × % complete (materials).

- Equivalent units for conversion = Units completed + Ending WIP units × % complete (labor and overhead).

- Cost per equivalent unit = (Beginning WIP cost + Costs added) ÷ Equivalent units.

- Assign costs to completed units and to ending WIP.

FIFO equivalent units:

- Exclude work done last period from current period equivalent units.

- Focus on current-period effort only.

- Gives a cleaner view of current period cost performance.

You can use either method and still nail how to calculate work in process ending inventory. Just stay consistent.

Overhead, Variances, and Spoilage

Overhead

- Use a predetermined overhead rate. For example, overhead per labor hour or per machine hour.

- Apply overhead to WIP as production happens.

- At period end, adjust under- or overapplied overhead. Small variances can go to cost of goods sold. Large ones may be prorated to WIP, finished goods, and COGS.

Spoilage and scrap

- Normal spoilage is part of product cost. It stays in WIP or finished goods.

- Abnormal spoilage is a period expense. It should not inflate inventory.

- Keep clean tags and reasons for each scrap event.

These items can swing your numbers. This is a key step in how to calculate work in process ending inventory with accuracy.

Common Mistakes to Avoid

I have seen these issues cause big swings at close. Watch for them.

- Mixing up materials purchased and materials used. Use only what went to production.

- Ignoring percent complete. Half-done units are not full cost units.

- Missing overhead adjustments. Underapplied overhead hides in WIP if you forget to true up.

- Counting finished units twice. Once they move to finished goods, they leave WIP.

- Poor cutoff. Late timecards and late material issues can distort WIP.

If you keep these in check, how to calculate work in process ending inventory becomes fast and clean.

Real-World Tips, Controls, and Audit-Ready Documentation

From my early plant closes, I learned that speed comes from routine and proof. These steps help.

- Do a fast floor walk near month end. Confirm what is still on the line.

- Use a WIP aging list. Old WIP often signals errors or stalled jobs.

- Lock production cutoff. Gather late tickets in a known bucket.

- Reconcile WIP to the general ledger. Tie to subledger or job list.

- Keep bills of materials tight. Wrong BOMs inflate materials used.

- Sample jobs. Check materials, labor hours, and overhead driver rates.

- Document assumptions on percent complete. Simple notes save painful audits.

With these habits, you can show anyone exactly how to calculate work in process ending inventory and why the number is right.

Simple Calculator Template You Can Use

Use this quick template in a spreadsheet or ERP export. It works for job order or process flows.

Inputs

- Beginning WIP

- Materials used

- Direct labor

- Overhead applied

- Units completed and transferred out

- Ending WIP units and percent complete (materials and conversion), if process costing

Process costing steps

- Compute equivalent units for materials and conversion.

- Compute cost per equivalent unit for materials and conversion.

- Assign costs to completed units and ending WIP.

Core plug

- Total manufacturing costs = Materials used + Direct labor + Overhead applied

- COGM = Cost assigned to completed units

- Ending WIP = Beginning WIP + Total manufacturing costs − COGM

Use this each month, and you will master how to calculate work in process ending inventory with confidence.

Frequently Asked Questions of how to calculate work in process ending inventory

What is included in WIP inventory?

WIP includes direct materials, direct labor, and applied manufacturing overhead for unfinished goods. It excludes selling, general, and administrative costs.

How do equivalent units affect WIP?

Equivalent units convert partial work into full-unit terms. They let you assign fair costs to completed units and to ending WIP.

Should I use weighted-average or FIFO for WIP?

Both work. Weighted-average is simpler and smooths costs. FIFO shows current-period performance better, but needs tighter tracking.

How does overhead impact how to calculate work in process ending inventory?

Overhead is part of conversion cost. If it is under- or overapplied, adjust it at period end, or your WIP and margins will be off.

How often should I update WIP?

Update WIP at least monthly for financial closes. Many teams do weekly checks to spot issues early.

Can I automate how to calculate work in process ending inventory?

Yes. Most ERPs can compute equivalent units and apply overhead. Still review percent complete, cutoff, and variances.

What happens if spoilage is high?

Normal spoilage stays in product costs. Abnormal spoilage goes to expense. Track causes to cut waste and protect margins.

Conclusion

You now have the tools to measure WIP with clarity and speed. Use the core formula, apply percent complete when needed, and control overhead, spoilage, and cutoff. When you know how to calculate work in process ending inventory the right way, you get cleaner books and better production choices.

Put the template into your next close. Share this guide with your team, subscribe for more practical finance tips, and drop a comment with your toughest WIP challenge.